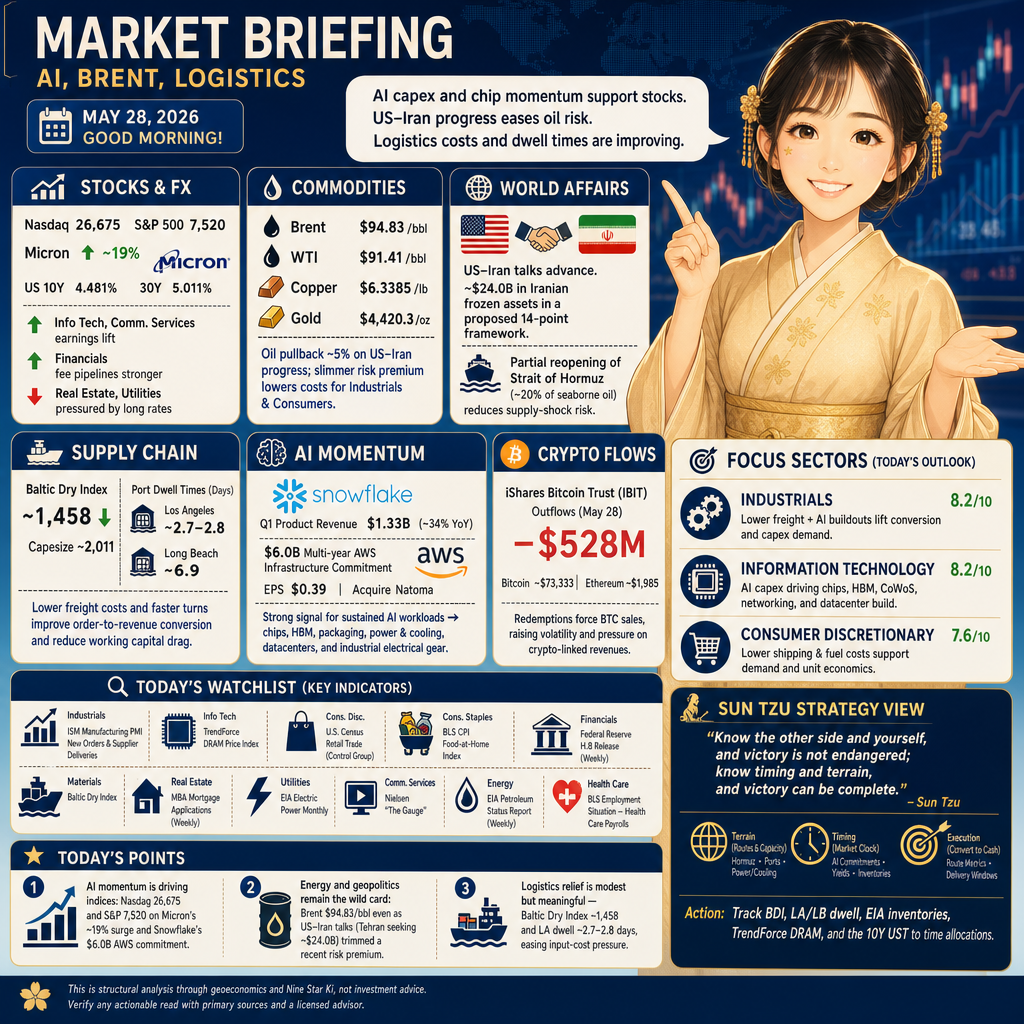

2026-05-28 Market Briefing| AI, Brent, Logistics

Good morning. AI capex and chip momentum are carrying the equity tape while diplomacy around Iran tempers the oil risk premium. Freight costs and port dwell times continue to ease, improving order‑to‑revenue conversion. Rate levels still cap long‑duration assets, and crypto outflows tighten a niche liquidity channel.

Stocks and FX

Nasdaq 26,675 and S&P 500 7,520 extended gains as Micron jumped ~19% and briefly touched ~$1.0 trillion in market value (Investing.com reporting Reuters). U.S. yields moderated with the 10‑year at 4.481% and the 30‑year at 5.011%, supporting growth multiples while keeping pressure on rate‑sensitives. The setup boosts Information Technology and Communication Services earnings expectations, while Financials see healthier fee pipelines and Real Estate/Utilities face valuation drag from elevated long rates.

Commodities

Brent at $94.83/bbl and WTI at $91.41/bbl remain volatile after an intraday pullback of about 5% on U.S.‑Iran progress headlines (MarketScreener reporting Reuters). Copper at $6.3385/lb and gold at $4,420.3/oz underscore dispersion across commodities. A slimmer oil risk premium eases transport and input costs for Industrials and Consumer sectors, while Energy revenues track crude with refining margins in focus.

World Affairs

$24.0 billion in Iranian frozen assets is reportedly part of a proposed 14‑point framework as U.S.‑Iran talks advance (Business Recorder/AFP). Markets are pricing a partial reopening of the Strait of Hormuz, which previously carried roughly 20% of seaborne oil, reducing supply‑shock risk and easing upside inflation pressure. That transmission can tighten credit spreads and stabilize issuance pipelines for Financials while trimming the Energy risk premium and shipping costs for Industrials.

Supply Chain

Baltic Dry Index fell to about 1,458 with Capesize near 2,011 (TradingView on Baltic Exchange data), while Port of Los Angeles import dwell averages ~2.7–2.8 days and Long Beach ~6.9 days (Hapag‑Lloyd ops). Softer bulk‑shipping costs and quicker turns lower delivered input prices and reduce working‑capital drag. Lead times improve for Materials and Industrials, and import‑reliant Consumer names gain inventory flexibility into summer.

AI

Snowflake posted $1.33 billion in Q1 product revenue (~34% yoy) and announced a $6.0 billion multi‑year AWS infrastructure commitment alongside EPS of $0.39 and a deal to acquire Natoma (BusinessWire/MarketScreener). The commitment signals sustained AI workloads, lifting demand for datacenter compute, networking, and software platforms. Transmission runs into chips, HBM (high‑bandwidth memory), advanced packaging capacity, and power/cooling availability, with knock‑on demand for industrial electrical gear and data‑center real estate.

Industry News

$528 million of outflows hit BlackRock’s iShares spot‑Bitcoin ETF on May 28 as Bitcoin traded near ~$73,333 and Ethereum around ~$1,985 (CoinDesk). ETF redemptions force underlying BTC sales, amplifying volatility and pressuring crypto‑linked trading revenues. Financials and select Information Technology/payment names with token‑related products or flows may see softer near‑term activity.

Industry Forecast

Today's Setup

May 28, 2026 is a Six White Metal (Roppaku Kinsei, 六白金星) day within a Five Yellow Earth month under Rikka (Beginning of Summer). Precision and central coordination favor operators that control routes and standards, so watch shipping costs, power/cooling constraints in data centers, and long‑rate financing as the levers that decide today’s margin and valuation moves.

Focus Sectors

- Industrials (8.2/10): BDI ~1,458 and LA/LB dwell at ~2.7–2.8/6.9 days are easing freight frictions, improving order‑to‑revenue conversion and reducing working‑capital drag. AI buildouts add a second pull‑through as Snowflake’s $6.0bn AWS commitment signals durable cloud/datacenter capex, lifting electrical equipment, thermal management, and precision components. Margin hold hinges on supplier deliveries and uptime. Risk: a reversal in Hormuz diplomacy could re‑inflate fuel/shipping costs; a sharp dollar move would pressure exports. Near term, supplier‑delivery metrics will steer beats.

- Information Technology (8.2/10): Micron’s ~19% surge and Snowflake’s $6.0bn AWS commitment reaffirm AI capex, sustaining demand for GPUs, HBM (high‑bandwidth memory), networking, and advanced packaging such as CoWoS (chip‑on‑wafer‑on‑substrate). Bottlenecks have shifted to packaging capacity and power/cooling availability; near‑term prints hinge on HBM/CoWoS supply and shipment timing. Export‑control changes remain a swing factor, and crypto ETF outflows can dampen token‑adjacent revenue. TrendForce DRAM prices will indicate cycle strength feeding AI servers.

- Consumer Discretionary (7.6/10): Logistics relief (BDI ~1,458; LA/LB dwell manageable) and a slimmer oil risk premium (Brent $94.83) lower freight and fuel costs, supporting unit economics in e‑commerce, travel, and experiential spend. An AI‑led equity tone lifts risk appetite, aiding conversion, while promotions and category mix drive margin dispersion. Rates still matter for big‑ticket items. Watch for any headline‑driven oil snap‑back that would quickly hit delivery and travel budgets; core retail control‑group sales will gauge demand breadth.

Watchlist

- Industrials: ISM Manufacturing PMI (Institute for Supply Management) — New Orders and Supplier Deliveries diffusion indexes for conversion and bottleneck stress.

- Information Technology: TrendForce DRAM contract price index (TrendForce — monthly DRAM pricing that tracks memory cycle strength feeding AI servers).

- Consumer Discretionary: U.S. Census Monthly Retail Trade Report — control‑group sales (ex‑autos, gas, building materials) for core discretionary demand.

- Consumer Staples: BLS CPI Food‑at‑Home index (Bureau of Labor Statistics — monthly grocery price inflation to gauge pricing power).

- Financials: Federal Reserve H.8 release (weekly assets and liabilities of U.S. commercial banks — loan growth, deposits, securities).

- Materials: Baltic Dry Index (The Baltic Exchange — composite cost of shipping dry bulk to gauge freight pressure on delivered input prices).

- Real Estate: MBA Mortgage Applications (Mortgage Bankers Association — weekly purchase/refi volumes and the 30‑year contract rate).

- Utilities: EIA Electric Power Monthly (U.S. Energy Information Administration — electricity demand growth by sector and generation mix).

- Communication Services: Nielsen ‘The Gauge’ (monthly U.S. TV viewing share across broadcast/cable/streaming — a proxy for ad inventory and engagement).

- Energy: EIA Weekly Petroleum Status Report (U.S. Energy Information Administration — crude/product inventories and refinery utilization).

- Health Care: BLS Employment Situation — Health care and social assistance payrolls (monthly job growth as a proxy for utilization and capacity).

Caveats

If U.S.‑Iran talks stall or a security incident constricts Hormuz, oil and freight costs could reset quickly and flip today’s logistics relief for Industrials and Consumer sectors. A surprise squeeze in HBM/advanced packaging or grid‑interconnect delays would slow the IT/datacenter cadence, and a material move in the 10‑year away from ~4.48% would reprice rate‑sensitives; seasonal shifts as Rikka wanes can also reweight energy and demand cues.

Sun Tzu Strategy View

Sun Tzu wrote: —— Know the other side and yourself, and victory is not endangered; know timing and terrain, and victory can be complete.

Today’s edge lies in reading both timing and terrain: the Hormuz chokepoint, port dwell times, and datacenter power/cooling capacity set the operating field, while AI commit timing and yield moves set the clock. Firms that position along these routes and sequence capital to delivery windows convert orders to cash and protect margins.

Action: Prioritize route‑ and capacity‑linked metrics (BDI, LA/LB dwell, EIA inventories, TrendForce DRAM) alongside the 10Y UST to time allocations and execution windows.

Today's Points

- AI momentum is driving indices: Nasdaq 26,675 and S&P 7,520 on Micron’s ~19% surge and Snowflake’s $6.0bn AWS commitment.

- Energy and geopolitics remain the wild card: Brent $94.83/bbl even as US‑Iran talks (Tehran seeking ~$24.0bn) trimmed a recent risk premium.

- Logistics relief is modest but meaningful — Baltic Dry Index ~1,458 and Port of Los Angeles dwell ~2.7–2.8 days, easing input‑cost pressure for Materials and Industrials.

This is structural analysis through geoeconomics and Nine Star Ki, not investment advice. Verify any actionable read with primary sources and a licensed advisor.