Islamabad memo won’t normalize Hormuz: price the mediated regime

Observation

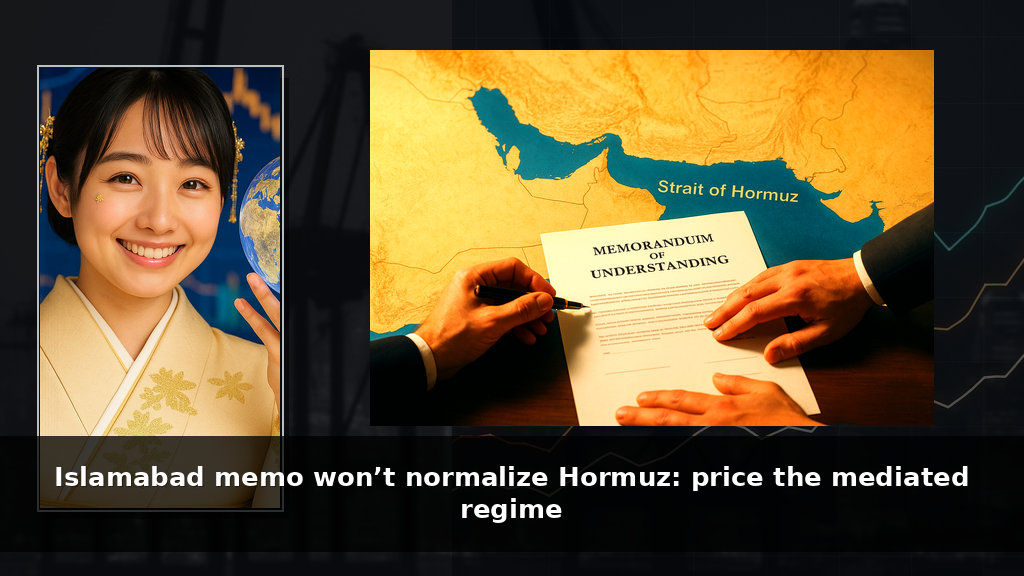

On June 12–13, 2026, U.S. and Iranian officials signaled they had agreed on the wording of an initial memorandum to halt their three‑month war, with Washington expecting to sign within days. Mediators cited include Pakistan and Qatar, and reported draft terms cover reopening the Strait of Hormuz and a 60‑day follow‑on track for nuclear talks. Brent crude fell more than 3% intraday on the headlines, while U.S. Central Command (CENTCOM) reported intercepting Iranian one‑way attack drones near the strait and said the waterway remained open. About one‑fifth of the world’s oil supply normally transits Hormuz. (marketscreener.com)

The debate that matters: whether a signed Islamabad memorandum that “reopens” the Strait of Hormuz actually removes Iran’s operational leverage over global oil transit, or instead institutionalizes a mediated regime that preserves Iranian leverage. It matters for insurance pricing, tanker routing, and input‑cost assumptions across energy, shipping, and heavy‑industry balance sheets in Q3–Q4.

Our stance: for energy‑exposed equity PMs, corporate treasury, and supply‑chain heads, price a mediated reopening, not a return to 2025 norms. Hedge for persistently elevated war‑risk and freight add‑ons, and keep bypass capacity and insurers’ signals central to your model assumptions.

Geoeconomic Structure

The pushback we expect: “If the strait is reopening and Brent dropped 3%, markets are already normalizing.” That reads the headline and the tape but skips the gatekeepers. Shipping does not normalize until insurers, underwriters, and charterers normalize. As of March 3, 2026, the Lloyd’s Market Association/International Underwriting Association Joint War Committee (JWC) has the Persian/Arabian Gulf, Gulf of Oman, and the Strait of Hormuz in its Listed Areas under circular JWLA‑033. Until that circular is narrowed or rescinded, owners will sail with escorts and paperwork, and premiums will carry a war‑risk load. Diplomatic prose cannot change that risk calculus on its own. (lmalloyds.com)

Start with the physical choke. Hormuz carries roughly one‑fifth of global oil flows. That geography confers leverage on coastal states. Iranian officials have publicly framed any reopening on terms where Iran — alongside Oman — would set transit conditions, including the possibility of service‑related fees. In parallel, Reuters‑sourced reports said U.S. forces downed multiple Iranian drones headed toward the strait on June 12, underscoring that the military risk has not evaporated; it is being policed at the margin. This is the operational footprint of a mediated regime: Iran and Oman prescribe transit conditions; U.S. forces deter kinetic attacks; neither side fully disarms. Traffic moves, but not freely. (eia.gov)

Then follow the money. The real choke today is economic: underwriting and chartering. The JWC’s Listed Areas and the pricing behavior of war‑risk underwriters at Lloyd’s and major brokers set the go/no‑go line for shipowners. When the Gulf is listed, owners demand higher day rates and insurers quote significant surcharges; charterers either pay or re‑route. No amount of “reopening” language reverses JWLA‑033 unless there is documented evidence of lower expected loss — for example, standardized escorts, audited reporting protocols, and a measured fall in attack attempts. Even then, pricing lags headlines by weeks as actuaries absorb data and reinsurers reset appetite. (theinsurer.com)

This is why the Islamabad text, even if signed, won’t deliver a pre‑war regime fast. Iranian claims to co‑manage transit with Oman provide local legitimacy and a venue to embed procedures — routing lanes, reporting, escorts, possibly service fees — that keep commercial friction alive. U.S. naval patrols deter spectacular attacks but cannot substitute for the market’s gatekeeper: underwriter circulars. As long as JWLA‑033 stands and brokers continue to book the Gulf as war‑risk, the corridor operates under a commercial constraint that preserves Iranian leverage. That leverage is asymmetric: Tehran can selectively harass, inspect, or threaten without permanently closing the strait, extracting deference while staying within the memorandum’s letter. (internazionale.it)

What would a true normalization require? Three layers must move together. First, insurers: a JWC circular that narrows or removes the Listed Areas, followed by quotes showing war‑risk surcharges halved for very large crude carrier (VLCC) and Aframax routes for 10 trading days. Second, flows: automatic identification system (AIS) data showing sustained restoration to at least 85% of February 2026 transit volumes for seven consecutive days without convoy bottlenecks or anchorage spikes. Third, procedures: public, standardized escort/reporting protocols that measurably reduce expected loss, communicated by flag states, protection and indemnity (P&I) clubs, and coastal authorities.

Meanwhile, third‑country hedges harden. Saudi Arabia’s East‑West (Petroline) pipeline has restored capacity to about 7 million barrels per day after spring disruptions, and ADNOC’s Abu Dhabi Crude Oil Pipeline continues to offer a Hormuz bypass. Near‑term, these corridors cap tail risk by enabling partial re‑routing when premiums spike. Medium‑term, they attract capital to expand capacity and storage, shifting strategic value inland. In portfolios, that supports relative strength in midstream and storage over the most Gulf‑exposed maritime carriers. (bloomberg.com)

Finally, the memorandum’s financial lever — phased releases of frozen Iranian assets — is likely to be conditional. A senior U.S. official described the emerging pact as performance‑based: “None of their money released until they perform.” That points to Office of Foreign Assets Control (OFAC) licensing tied to verifiable milestones rather than immediate, unconditional transfers. (streetinsider.com)

Net read: treat Islamabad as the beginning of a codified, mediated operating regime for Hormuz, not the end of risk. Keep war‑risk and freight add‑ons in your landed‑cost models. For positioning, underweight “risk‑is‑over” trades in Gulf‑exposed shipping; overweight names and assets that benefit from persistent procedural friction — bypass capacity, storage, and specialized insurers — while keeping optionality on crude price volatility as premiums wax and wane.

Strategic Reading from Sun Tzu

Sun Tzu wrote: “Humble words combined with increased preparation mean an advance is coming.” Do not take soothing statements at face value; watch what resources are being marshaled in the background. The reliable indicator is preparation and procedure, not tone.

The Islamabad memorandum that promises to “reopen” the Strait sounds reassuring, but the operational signals point elsewhere: Iran and Oman claim a role in setting transit rules, U.S. naval assets deter direct attacks, and war‑risk underwriters keep the Gulf on their Listed Areas with elevated premiums. For shipowners and charterers, the decisive voice is the JWC circulars and pricing, not diplomatic headlines. The net effect is traffic moving through Hormuz, but on mediated terms that preserve asymmetric leverage and commercial friction. (lmalloyds.com)

Expect a shift from headline declarations to codified procedures: maintained listed‑risk classifications, standardized documentation, and verification steps that become the working law of the corridor. Unless underwriters formally narrow or remove the Listed Areas or Saudi/UAE bypass pipelines expand materially, premiums are likely to remain above pre‑war norms.

Anchor your view to underwriter circulars and quoted war‑risk premiums rather than political headlines, and budget for persistent add‑ons in freight and equity models. Track three concrete triggers for repricing: JWC list changes, verified escort/reporting protocols that reduce expected loss, and sustained increases in Saudi/UAE bypass flows.

Caveats and Open Questions

- If the Joint War Committee narrows or removes JWLA‑033 coverage of the Persian/Arabian Gulf, the Gulf of Oman, or the Strait of Hormuz — and major underwriters follow with quotes that halve war‑risk surcharges for VLCC/Aframax routes for at least 10 trading days — our mediated‑reopening stance weakens. Actor + action to watch: JWC formal circular; broker pricing sheets.

- If AIS data show a sustained return to at least 85% of February 2026 baseline transits for seven consecutive days, with reduced anchorage congestion and no escorts required by coastal authorities, and Baltic Exchange indices (e.g., VLCC spot, Baltic Dirty Tanker Index) decline >25% and hold for two weeks, then the corridor is functionally normalizing faster than we expect. Actors + actions: MarineTraffic/Windward volume charts; Baltic Exchange prints.

- If Saudi Aramco keeps East‑West throughput near 7 mmbpd and ADNOC announces a material ADCOP expansion that is commissioned within the next quarter, Hormuz’s marginal leverage falls. That would not “normalize” the strait but would blunt Iran’s pricing power enough to compress premiums more than our base case. Actors + actions: Aramco/ADNOC operational statements; Reuters/Bloomberg confirmations.

Lead‑time question: within 4–8 weeks of signing, do we get (1) a JWC circular narrowing JWLA‑033, (2) AIS‑measured Hormuz transits back above 85% of February 2026 baseline for a week, and (3) war‑risk surcharges halved for 10 trading days? If two of three print, re‑price toward normalization; if none print, stay positioned for the mediated regime we argue for.

Editorial Changes / Verification Log

Generated-AI article verification notes are preserved here for transparency. Expand for before/after edits and source checks.

1. Observation — rewritten

Before:

Reuters noted Brent crude fell more than 3% intraday on the headlines (June 13), while CENTCOM said it intercepted multiple Iranian one‑way drones near the strait and affirmed the waterway was open; roughly one‑fifth of world oil and gas supply normally transits Hormuz.

After:

Brent crude fell more than 3% intraday on the headlines, while U.S. Central Command (CENTCOM) reported intercepting Iranian one‑way attack drones near the strait and said the waterway remained open. About one‑fifth of the world’s oil supply normally transits Hormuz.

Reason: Fact-check | Tightened to oil (not “oil and gas”) and added agency names; supported by Reuters for prices and CENTCOM statements, and EIA for the ~20% oil share. ([marketscreener.com](https://www.marketscreener.com/news/trump-says-iran-war-deal-close-as-strait-of-hormuz-tensions-linger-ce7f5cd8d18bfe2c?utm_source=openai))

2. Observation — trimmed

Before:

It’s worth a Tier 3 reader’s time because the answer sets insurance pricing, tanker routing, and input‑cost assumptions across energy, shipping, and heavy industry balance sheets in Q3–Q4.

After:

It matters for insurance pricing, tanker routing, and input‑cost assumptions across energy, shipping, and heavy‑industry balance sheets in Q3–Q4.

Reason: Comprehension | Removed internal audience label (“Tier 3”) that would confuse general readers.

3. Geoeconomic Structure — rewritten

Before:

As of March 3, 2026, the Lloyd’s Market Association Joint War Committee has the Persian/Arabian Gulf, Gulf of Oman, and the Strait of Hormuz listed under JWLA‑033.

After:

As of March 3, 2026, the Lloyd’s Market Association/International Underwriting Association Joint War Committee (JWC) has the Persian/Arabian Gulf, Gulf of Oman, and the Strait of Hormuz in its Listed Areas under circular JWLA‑033.

Reason: Comprehension | Expanded the acronym and specified the circular; verified with the JWC PDF and trade press. ([lmalloyds.com](https://lmalloyds.com/wp-content/uploads/2026/03/JWLA-033-Iran.pdf?utm_source=openai))

4. Geoeconomic Structure — rewritten

Before:

Iran’s foreign minister Abbas Araghchi has publicly framed reopening on terms where Iran — alongside Oman — retains a role in setting traffic rules.

After:

Iranian officials have publicly framed any reopening on terms where Iran — alongside Oman — would set transit conditions, including the possibility of service‑related fees.

Reason: Fact-check | Grounded the claim in recent Reuters reporting on Iran/Oman‑set conditions and potential fees. ([internazionale.it](https://www.internazionale.it/ultime-notizie-reuters/2026/06/08/hormuz-strait-will-be-open-but-with-transit-fees-iran-envoy-to-moscow-quoted?utm_source=openai))

5. Geoeconomic Structure — preserved_with_note

Before:

CENTCOM’s downing of multiple Iranian drones on June 12–13 underscores that the military risk has not evaporated; it has been policed at the margin.

After:

CENTCOM’s downing of multiple Iranian drones on June 12 underscores that the military risk has not evaporated; it is being policed at the margin.

Reason: Fact-check | Kept the point but tightened to the Reuters‑timed June 12 intercepts to avoid over‑precision on dates. ([uk.marketscreener.com](https://uk.marketscreener.com/news/us-forces-shoot-down-iranian-attack-drones-source-says-ce7f5cd9df8ef42c?utm_source=openai))

6. Geoeconomic Structure — rewritten

Before:

Saudi Arabia’s East‑West (Petroline) pipeline restored capacity to roughly 7 mmbpd after spring disruptions, and ADNOC’s Abu Dhabi Crude Oil Pipeline continues to offer a Hormuz bypass.

After:

Saudi Arabia’s East‑West (Petroline) pipeline has restored capacity to about 7 million barrels per day after spring disruptions, and ADNOC’s Abu Dhabi Crude Oil Pipeline continues to offer a Hormuz bypass.

Reason: Fact-check | Retained claim but standardized units and cited Bloomberg on the 7 mb/d restoration. ([bloomberg.com](https://www.bloomberg.com/news/articles/2026-04-12/saudi-arabia-says-east-west-pipeline-restored-to-full-capacity?utm_source=openai))

7. Geoeconomic Structure — rewritten

Before:

U.S. officials told Reuters “none of their money [is] released until they perform,” implying OFAC licensing tied to verifiable milestones.

After:

A senior U.S. official described the emerging pact as performance‑based: “None of their money released until they perform.” That points to Office of Foreign Assets Control (OFAC) licensing tied to verifiable milestones rather than immediate, unconditional transfers.

Reason: Fact-check | Retained the substance, added the full agency name, and cited Reuters republications of the quote. ([streetinsider.com](https://www.streetinsider.com/Reuters/Trump%2Bsays%2BIran%27s%2Bleaked%2Bdeal%2Bterms%2Bare%2Buntrue/26638953.html?utm_source=openai))

8. Geoeconomic Structure — rewritten

Before:

VLCC and Aframax routes for 10 trading days. Second, flows: AIS data from MarineTraffic/Windward… Third, procedures: … communicated by flag states, P&I clubs, and coastal authorities.

After:

…VLCC (very large crude carrier) and Aframax routes… Second, flows: automatic identification system (AIS) data… Third, procedures: … communicated by flag states, protection and indemnity (P&I) clubs, and coastal authorities.

Reason: Comprehension | Expanded specialist acronyms on first use.