The Industrial Structure After Hormuz (Part 1)

What Fatih Birol’s Warning Revealed

In May 2026, Fatih Birol, executive director of the International Energy Agency, warned that oil markets were approaching dangerous territory. His warning did not point only to higher crude prices. The issue is not simply more expensive gasoline. Instability in the Strait of Hormuz strikes the supply network itself, spanning crude oil, LNG, naphtha, LPG, fertilizer, aviation fuel, maritime transport, insurance, inventories, electricity, chemical feedstocks, and national industrial policy.

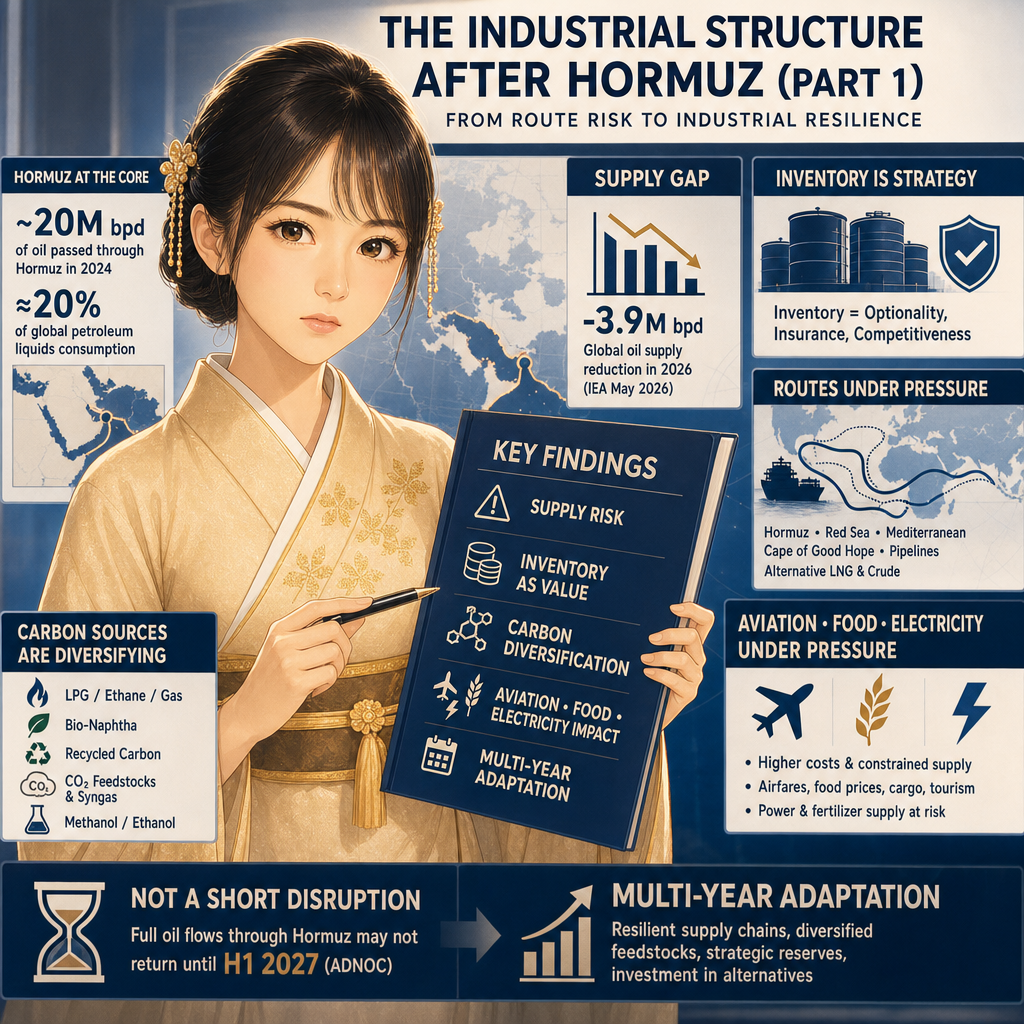

The Strait of Hormuz is not just one route in global energy logistics. According to the U.S. Energy Information Administration, about 20 million barrels per day of oil passed through the Strait of Hormuz in 2024, equal to roughly 20% of global petroleum liquids consumption. Much of that crude oil, condensate, and LNG moves to Asia. Industrial economies such as China, India, Japan, and South Korea remain structurally exposed to this strait.

The central question is not only whether the strait has fully closed. The deeper issue is that Hormuz no longer functions as a route that firms can assume is naturally available. The IEA’s May 2026 Oil Market Report stated that production in Gulf countries affected by a closure of the Strait of Hormuz was 14.4 million barrels per day below prewar levels, and projected that global oil supply in 2026 would fall by an average of 3.9 million barrels per day.

This is not a temporary price fluctuation. It means that the implicit condition behind modern industry, “if it can be bought, it will arrive,” has been shaken.

Uninterrupted Operation Becomes Value, Not Price Alone

Global industry has long depended on the premise that energy available for purchase also arrives. Crude oil and LNG from the Middle East pass through Hormuz, move by tanker to Asia and Europe, and become fuels, naphtha, resins, fibers, solvents, fertilizers, and electronic materials at refineries and petrochemical complexes. As long as that flow remains stable, companies can keep inventories thin, stretch supply chains over long distances, and shift production toward cheaper procurement sources.

Once Hormuz becomes unstable, that premise breaks. Buyers can offer more dollars and increase orders. Dollars do not grow new oil fields by the next day. Tankers, ports, insurance underwriting capacity, pipelines, refining capacity, and chemical plants expand only at the speed of the physical world. Demand-side money moves quickly, while supply-side capacity moves slowly. This speed gap raises prices, changes investment decisions, and shifts the industrial center of gravity.

The first thing that changes is the meaning of inventory. In the age of efficiency, inventory was a cost. In the post-Hormuz age, inventory becomes optionality, insurance, and in some cases competitiveness itself. Companies face a different question: not how cheaply they can avoid holding stock, but how long they can continue operating without stopping. The combination of national reserves, private reserves, corporate inventories, and alternative procurement becomes an institutional buffer against cascading shutdowns, not a temporary emergency response.

Logistics follow the same logic. When Hormuz is unavailable or difficult to use, the Red Sea, the Mediterranean, the Cape of Good Hope, pipelines, non-Middle Eastern crude, and alternative LNG procurement all gain importance. None is a perfect substitute. According to Reuters, ADNOC’s chief executive said that even if the conflict ended early, full oil flows through the Strait of Hormuz may not return until the first half of 2027.

This is not a disruption measured in weeks. It is an event that changes corporate procurement planning and government energy policy over a multiyear horizon.

Petrochemicals Ask Where Carbon Comes From

A deeper change appears in petrochemicals. When crude prices rise, many people first think of gasoline and diesel. In modern industry, however, crude oil is not only something to burn. Through naphtha, it becomes ethylene, propylene, BTX (benzene, toluene, xylene), synthetic resins, synthetic fibers, rubber, paints, adhesives, solvents, agrochemicals, pharmaceutical intermediates, and electronic materials. In its May 2026 Oil Market Report, the IEA identified petrochemicals and aviation as among the sectors currently most affected.

The industrial question shifts from “where to buy crude oil” to “where to obtain carbon.” Petrochemicals require carbon. This is therefore not simple de-oiling. It is a move to weaken one-sided dependence on crude-derived naphtha and diversify carbon sources into LPG, ethane, natural gas, bio-naphtha, waste-plastic pyrolysis oil, methanol, ethanol, CO2-derived feedstocks, and syngas. It is environmental policy and, at the same time, feedstock diversification as supply security.

This transition does not occur immediately as full substitution. Bio-based feedstocks do not yet provide enough volume or cost competitiveness to replace all commodity plastics. Large-scale direct production of ethylene from CO2 faces severe constraints in electricity, hydrogen, catalysts, equipment, and separation processes. The first advances come from blending alternative feedstocks into existing equipment, replacing feedstocks in high-value products, and introducing new inputs into applications that can absorb premiums through brand value or regulatory compliance.

Food packaging, cosmetics containers, medical materials, electronic materials, and specialty resins can absorb feedstock premiums more easily. Low-value mass plastics face stronger price pressure. In those areas, demand restraint, material substitution, and recycled materials gain ground. Post-Hormuz petrochemicals move away from mass production premised on cheap naphtha and toward an industry that selects, blends, and allocates carbon sources by application.

Supply Anxiety Spreads to Aviation, Food, and Electricity

Aviation has the same structure. Aviation fuel is hard to replace, and electrification remains limited over the short and medium term. When price pressure and supply constraints intensify, airfares, flight frequencies, routes, air cargo rates, tourism, and business travel are affected first. The IEA projected that global oil demand in 2026 would decline by 420,000 barrels per day year on year, with a particularly sharp fall of 2.45 million barrels per day in the second quarter, in its May 2026 Oil Market Report.

This is not merely savings. It means selection begins: which movements to preserve, which to cut, which cargo to prioritize, and which transport to defer. Aviation becomes a site where economic priorities become visible, not only a sector exposed to fuel prices.

Agriculture and food also come under pressure. Crude oil and natural gas connect to farm machinery fuel, transport, refrigeration, packaging materials, and fertilizer. Hormuz instability spreads not only through crude prices, but through LPG, naphtha, ammonia, urea, marine fuel, and container freight rates. The post-Hormuz condition is therefore a fuel crisis and a crisis of food costs and living costs.

Power systems also change. Even in countries with low shares of oil-fired generation, the value of LNG, coal, nuclear power, renewable energy, storage batteries, transmission grids, and demand response shifts. The longer uncertainty over Middle Eastern supply persists, the more renewable energy and nuclear power are revalued not only as decarbonization policy, but as security policy that reduces dependence on imported-fuel chokepoints. Fatih Birol has also stated that the present crisis is prompting countries to reassess energy sources and accelerating a shift toward renewable energy and nuclear power, as reported by The Guardian.

Factory Location and Finance Also Change

The conditions for manufacturing location also change. Until now, labor costs, tax systems, ports, supplier networks, and proximity to markets formed the main criteria for factory location. After Hormuz, another condition gains weight: whether energy and raw materials can keep flowing.

Even low labor costs lose force if electricity, fuel, chemical feedstocks, fertilizer, packaging materials, and transport insurance become unstable. Future manufacturing sites place greater emphasis on multiple fuel procurement routes, stable electricity supply, port redundancy, storage capacity, domestic or nearby refining and chemical bases, and access to alternative feedstocks. The value shifts from making goods in cheap places to making goods in places that do not stop.

The financial dimension also changes. When crude prices rise, central banks grow alert to inflation and become cautious about rate cuts. Higher interest rates, however, do not increase oil fields. Instead, high rates raise the investment cost of upstream development, refining, alternative fuels, chemical feedstock conversion, renewable energy, and nuclear power. The Financial Times reported that higher energy prices caused by the Iran crisis led to lower European growth forecasts and higher inflation forecasts (Financial Times).

This is the difficulty of inflation driven by physical constraints. Monetary policy that cools demand does not quickly increase tankers, pipelines, refineries, chemical plants, or transmission grids. When supply anxiety creates inflation, the boundary between monetary policy and industrial policy becomes blurred.

Government Becomes an Allocator Outside the Market

The role of government also changes. In normal times, higher prices reduce demand and increase supply through the market. When a chokepoint such as Hormuz becomes unstable, markets alone cannot complete the adjustment. Governments combine reserve releases, alternative procurement, fuel subsidies, demand restraint, delayed refinery maintenance, priority management of aviation fuel, biofuel blending, nuclear utilization, temporary relaxation of coal use, and faster renewable deployment.

This does not reject markets. It addresses how to allocate market price signals under physical supply constraints. The question becomes which uses receive scarce fuel, routes, and time. The post-Hormuz government becomes not only the buyer of last resort in crisis, but also an allocator of time, routes, fuels, and demand.

As a result, industrial structure moves toward embedding redundancy as value, not only efficiency. The old optimization model was to produce in cheap locations, ship through cheap routes, reduce inventories, and procure only when needed. Value now shifts toward maintaining multiple routes even at higher cost, holding inventories, preserving minimum domestic or nearby production capacity, and diversifying feedstocks.

This is not simple conservatism. It is a change in industrial design philosophy. What occurred in semiconductors is spreading to energy, chemicals, fertilizers, materials, logistics, aviation, food packaging, and pharmaceutical intermediates. The definition of competitiveness shifts away from “cheap is enough,” “it should arrive,” and “outsourcing suffices,” and toward “it does not stop,” “it can detour,” “it can substitute,” and “it can allocate by priority.”

The Indicators to Watch Are Not Only Crude Prices

The essence of the post-Hormuz condition is not high crude prices. It is the transition from an industrial structure premised on stable supply to one premised on supply anxiety.

For that reason, crude prices alone are insufficient indicators. Naphtha prices, LPG prices, aviation fuel inventories, refining margins, tanker freight rates, marine insurance premiums, remaining days of strategic reserves, alternative procurement ratios, petrochemical operating rates, fertilizer prices, bio-naphtha premiums, waste-plastic pyrolysis oil prices, LNG spot prices, nuclear operating rates, and the speed of renewable deployment all require attention. Crude prices are the entry point; structural change appears downstream.

Crude prices may eventually fall. Prices decline when demand breaks, supply returns, and the economy slows. Yet the behavior of companies and states that experience Hormuz instability does not fully return to its previous form. Reserves become thicker. Procurement sources split. Feedstocks diversify. Power systems are reviewed. Logistics routes gain redundancy. Refining capacity and chemical bases are treated as security assets. Decisions of this kind, once started, are not easily reversed.

When buyers offer more dollars, the number of buyers increases immediately. Dollars do not grow oil fields by the next day. Tankers, pipelines, refineries, and chemical plants expand only at the speed of the physical world. This speed gap raises prices, changes investment decisions, moves governments, and remakes industrial structure.

The post-Hormuz condition is not a story about geopolitical risk in a distant strait. It is the world after the premise on which modern industry has relied, “cheap from far away, delivered when needed,” has been shaken. The next stage of industrial competitiveness is not determined by access to cheap crude oil, but by whether an economy has a structure that keeps fuel, electricity, chemical feedstocks, logistics, and food supply moving even when crude oil becomes unstable.

In Part 2, the focus turns to how governments and producers are buying time and reorganizing routes and demand in response to this supply anxiety.

Editorial Changes / Verification Log

Generated-AI article verification notes are preserved here for transparency. Expand for before/after edits and source checks.

1. (unspecified section) — other

Before:

According to the U.S. Energy Information Administration, about 20 million barrels per day of oil passed through the Strait of Hormuz in 2024, equal to roughly 20% of global petroleum liquids consumption. Much of that crude oil, condensate, and LNG moves to Asia. Industrial economies such as China, India, Japan, and South Korea remain structurally exposed to this strait. [U.S. Energy Information Administration](https://www.eia.gov/todayinenergy/detail.php?id=65504&utm_source=chatgpt.com)

After:

According to the [U.S. Energy Information Administration](https://www.eia.gov/todayinenergy/detail.php?id=65504&utm_source=chatgpt.com), about 20 million barrels per day of oil passed through the Strait of Hormuz in 2024, equal to roughly 20% of global petroleum liquids consumption. Much of that crude oil, condensate, and LNG moves to Asia. Industrial economies such as China, India, Japan, and South Korea remain structurally exposed to this strait.

Reason: Moved the citation onto a natural anchor phrase and removed a trailing standalone link for cleaner flow and compliance with citation formatting.

2. (unspecified section) — sentence_split

Before:

This does not reject markets. It addresses the allocation of market price signals under physical supply constraints: which uses receive scarce fuel, routes, and time.

After:

This does not reject markets. It addresses how to allocate market price signals under physical supply constraints. The question becomes which uses receive scarce fuel, routes, and time.

Reason: Split a long sentence and clarified the referent to improve readability without changing meaning.

3. (unspecified section) — other

Before:

Reuters reported that ADNOC’s chief executive said that even if the conflict ended early, full oil flows through the Strait of Hormuz may not return until the first half of 2027. [Reuters](https://www.reuters.com/business/energy/no-full-hormuz-flows-until-first-half-2027-uaes-oil-giant-says-2026-05-21/?utm_source=chatgpt.com)

After:

According to [Reuters](https://www.reuters.com/business/energy/no-full-hormuz-flows-until-first-half-2027-uaes-oil-giant-says-2026-05-21/?utm_source=chatgpt.com), ADNOC’s chief executive said that even if the conflict ended early, full oil flows through the Strait of Hormuz may not return until the first half of 2027.

Reason: Anchored the link to the source name within the sentence for smoother narrative flow.

4. (unspecified section) — other

Before:

In its May 2026 report, the IEA identified petrochemicals and aviation as among the sectors currently most affected. [IEA May 2026 report PDF](https://iea.blob.core.windows.net/assets/2b89a47b-34a2-40e0-90ff-68f7ccd80715/-13MAY2026__OilMarketReport_publicversion.pdf?utm_source=chatgpt.com)

After:

In its [May 2026 Oil Market Report](https://iea.blob.core.windows.net/assets/2b89a47b-34a2-40e0-90ff-68f7ccd80715/-13MAY2026__OilMarketReport_publicversion.pdf?utm_source=chatgpt.com), the IEA identified petrochemicals and aviation as among the sectors currently most affected.

Reason: Placed the link on a natural anchor phrase and tightened the sentence.

5. (unspecified section) — gloss_added

Before:

Through naphtha, it becomes ethylene, propylene, BTX, synthetic resins, synthetic fibers, rubber, paints, adhesives, solvents, agrochemicals, pharmaceutical intermediates, and electronic materials.

After:

Through naphtha, it becomes ethylene, propylene, BTX (benzene, toluene, xylene), synthetic resins, synthetic fibers, rubber, paints, adhesives, solvents, agrochemicals, pharmaceutical intermediates, and electronic materials.

Reason: Added a brief parenthetical gloss to prevent a technical term from blocking comprehension.