2026-06-01 Market Briefing| H200 approvals, Hormuz reopening, freight squeeze

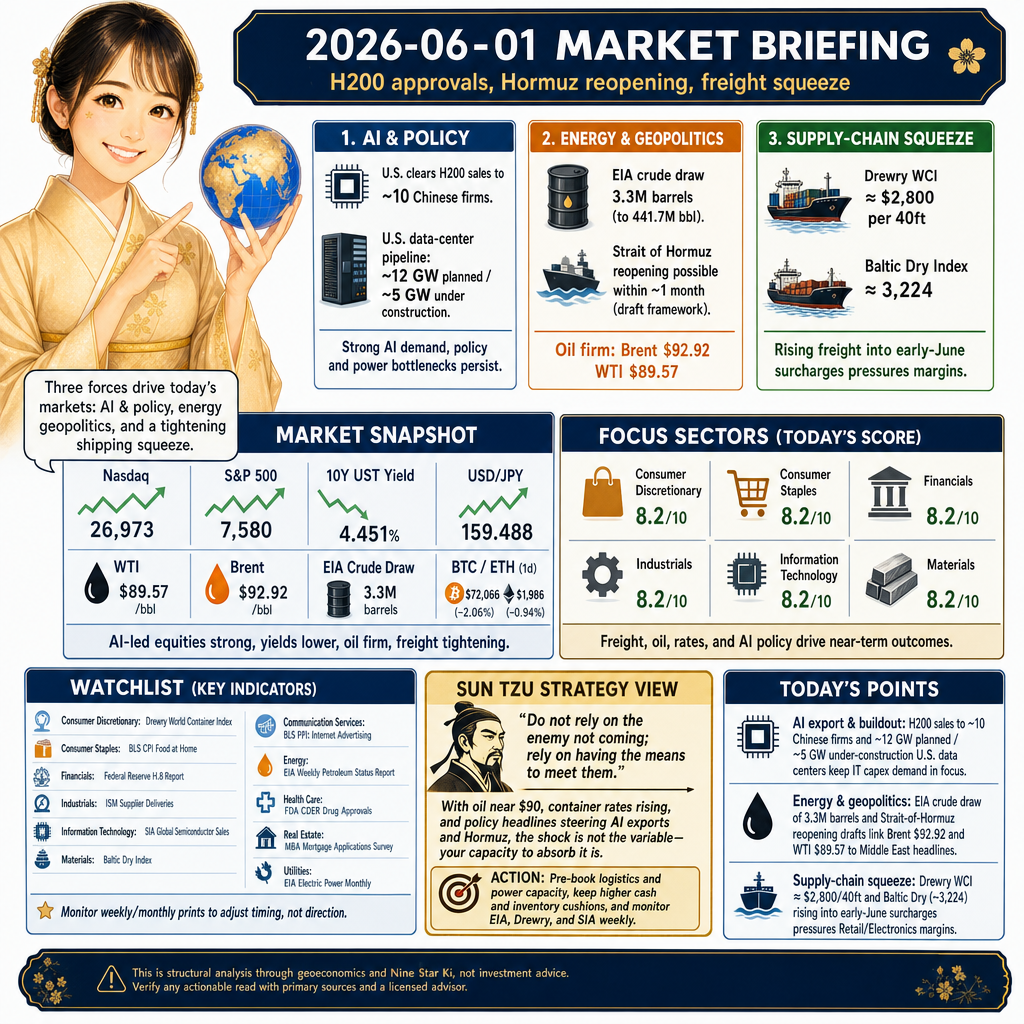

Good morning. Nasdaq 26,973 and the S&P 500 7,580 capped a multi-day AI-led run as the 10-year U.S. Treasury yield eased to 4.451%. WTI $89.57 and Brent $92.92 held firm after a 3.3M-bbl EIA draw, while container and dry-bulk rates tightened (WCI ≈ $2,800/40ft; BDI ≈ 3,224). Policy gates steer today’s tape: reported H200 export clearances, a possible Hormuz reopening within ~1 month, and early-June freight surcharges connect equity, energy, and supply-chain costs.

Stocks and FX

26,973 on the Nasdaq and 7,580 on the S&P 500 into the June 1 open tracked a six-day decline in the 10Y UST to 4.451% (AP). USD/JPY printed 159.488 as AI- and semiconductor-led gains lifted multiples and risk appetite. Lower yields support growth-stock valuations and deal activity, while pressuring bank net interest margin; a strong dollar can tighten imported-margin math for U.S. retailers and device assemblers.

Commodities

WTI $89.57/bbl and Brent $92.92/bbl followed a 3.3M-bbl U.S. crude draw to 441.7M bbl (EIA Weekly Petroleum Status Report). The near-term tightness sustains fuel and feedstock costs for Industrials and Materials and raises freight surcharges that feed into Retail and Electronics landed prices. Any confirmation of Middle East de-escalation could trim the risk premium quickly.

World Affairs

≈1 month is the indicated timetable for a Strait of Hormuz reopening under a reported draft framework (StreetInsider republishing Reuters). With Brent at $92.92 and WTI at $89.57, headline risk around ceasefire extensions drives crude and shipping premia. A credible reopening would ease Energy input uncertainty and reduce insurance and delay risk for Transport and Industrials.

Supply Chain

≈$2,800 per 40ft on Drewry’s World Container Index and a ~3,224 Baltic Dry Index print signal tightening into early-June surcharges (Daily Cargo News). Higher container and bulk rates lift landed costs and lengthen booking lead times for apparel, electronics, and chemicals, while supporting pricing for carriers and some freight-forwarders. Expect inventory planning to skew earlier with higher safety stock.

AI

10 approved Chinese buyers for Nvidia’s H200 and a U.S. AI data-center pipeline of ≈12 GW planned with ≈5 GW under construction anchor demand (Newsquawk summarizing Reuters; Bloomberg-derived data). That supports semiconductor and server order books but collides with power-equipment bottlenecks and higher ocean freight. Policy headlines and grid access timing will dominate near-term delivery and revenue recognition for AI suppliers.

Industry News

BTC $72,066 (−2.06% 1d) and ETH $1,986 (−0.94% 1d) traded on low spot volumes with crypto ETF outflows flagged by exchange briefs (CoinDesk, MEXC commentary). The dispersion versus record equities channels flows toward AI-led names while weighing on crypto-exposed payments and exchange revenues in Information Technology and Financials.

Industry Forecast

Today's Setup

June 1 sits under Day-star One White Water (Ippaku Suisei, 一白水星) at the Center (Chūkyū, 中宮), with the month in Five Yellow Earth, and Boshu (Grain in Ear) due on June 6. Translation: policy gatekeepers shape how fast information, capital, and goods flow — shipping costs, the rate path, and AI export policy dominate costs, financing conditions, and supply constraints today.

Focus Sectors

- Consumer Discretionary (8.2/10): $2,800 per 40ft on Drewry’s WCI and early-June surcharges raise landed costs for retailers and apparel assemblers, pressuring gross margins (Daily Cargo News). A 4.451% 10Y supports credit-sensitive demand and promo ROI as AI wealth effects lift the tape (AP). Risk: another freight leg higher or oil near WTI $89.57/Brent $92.92 may outpace pricing power into back-to-school; a yield rebound would raise auto and big-ticket financing costs just as inventory arrives.

- Consumer Staples (8.2/10): WCI ≈ $2,800 and BDI ≈ 3,224 lift logistics and packaging costs, but shelf-stable portfolios and contracts aid pass-through (Daily Cargo News). Oil firmness after a 3.3M-bbl EIA draw adds a manageable energy headwind (EIA). Defensiveness holds while surcharges stick; watch retailer resistance to list-price hikes if freight stays elevated and the equity-duration bid fades on a rate backup.

- Financials (8.2/10): A 4.451% 10Y compresses net interest margins but supports issuance and trading fee pools as equities rally (AP). Crypto liquidity remains thin with multi-day ETF outflows, pressuring exchange and payments niches (CoinDesk/MEXC). Constructive intermediation and wealth flows offset some NIM drift; key risks are a sharp rate backup hitting bond portfolios and a prolonged crypto slump cutting transaction volumes.

- Industrials (8.2/10): WCI ≈ $2,800 and BDI ≈ 3,224 support carriers and some forwarders but raise inputs for import-heavy manufacturers (Daily Cargo News). AI build-out stays firm with ≈12 GW planned vs ≈5 GW under construction, keeping electrical-equipment books tight (Bloomberg-derived). A credible Hormuz reopening within ~1 month would trim shipping premia (Reuters via StreetInsider). Watch transformer/switchgear lead times; fuel and materials costs track EIA’s tight crude balances.

- Information Technology (8.2/10): U.S. approvals for Nvidia H200 to ~10 Chinese firms plus a ≈12 GW/≈5 GW AI data-center pipeline extend chip and server demand (Newsquawk; Bloomberg-derived). Tighter ocean freight complicates component procurement timing (Drewry/BDI). Upside hinges on export-policy stability and power-equipment deliveries; reversals in approvals or grid delays can defer data-center ramps and vendor revenue.

- Materials (8.2/10): A ~3,224 Baltic Dry Index supports miners’ realized pricing, while container tightness raises input costs for chemicals and packaging (Daily Cargo News). Oil’s 3.3M-bbl EIA draw underpins feedstocks; a possible Hormuz reopening could unwind part of the energy/shipping premium (EIA; Reuters via StreetInsider). Near-term P&L sensitivity is high to freight and crude prints; contract structures will determine pass-through.

Watchlist

- Consumer Discretionary: Drewry World Container Index (weekly global 40ft container rates, published by Drewry).

- Consumer Staples: BLS CPI Food at Home index (monthly U.S. grocery price inflation, Bureau of Labor Statistics).

- Financials: Federal Reserve H.8 report (weekly U.S. commercial bank assets and loan growth, Board of Governors of the Federal Reserve System).

- Industrials: ISM Manufacturing Supplier Deliveries index (monthly measure of supplier lead times, Institute for Supply Management).

- Information Technology: SIA Global Semiconductor Sales (monthly worldwide chip sales, Semiconductor Industry Association).

- Materials: Baltic Dry Index (daily composite dry-bulk shipping rates, published by the Baltic Exchange).

- Communication Services: BLS Producer Price Index: Internet advertising, except search (monthly pricing for digital ad inventory, Bureau of Labor Statistics).

- Energy: EIA Weekly Petroleum Status Report (weekly U.S. crude inventories and refinery utilization, U.S. Energy Information Administration).

- Health Care: U.S. FDA CDER monthly drug approvals (count of new molecular entity approvals, U.S. Food and Drug Administration).

- Real Estate: Mortgage Bankers Association Weekly Mortgage Applications Survey (weekly U.S. purchase and refinance loan demand).

- Utilities: EIA Electric Power Monthly (U.S. capacity additions, generation mix, and retail electricity sales, U.S. Energy Information Administration).

Caveats

The solar term shifts to Boshu on June 6, which can rebalance today’s Center-weighted flow toward execution and planting—expect a tone change mid-window. Several sectors score well despite freight and oil headwinds; if policy or chokepoint news breaks the other way, Five-Element support may not cushion near-term tape. Freight (WCI/BDI) and H200 approval reports are volatile and partially second-hand; delivery and rate resets can move faster than weekly data.

Sun Tzu Strategy View

Sun Tzu wrote: —— Do not rely on the enemy not coming; rely on having the means to meet them.

With oil near $90, container rates rising, and policy headlines steering AI exports and Hormuz, the shock is not the variable—your capacity to absorb it is. Build buffers in freight, power, and financing so approvals, surcharges, or reopenings do not dictate outcomes.

Action: Pre-book critical logistics and power capacity, keep higher cash and inventory cushions, and monitor EIA, Drewry, and SIA prints weekly to adjust timing, not direction.

Today's Points

- AI export and buildout: U.S. clearance of H200 sales to ~10 Chinese firms plus a ~12 GW planned / ~5 GW under-construction U.S. data-center pipeline keeps IT capex demand (semiconductors, servers) in focus.

- Energy & geopolitics: an EIA crude draw of 3.3M barrels (to 441.7M bbl) and Strait-of-Hormuz reopening drafts link Brent $92.92 and WTI $89.57 to evolving Middle East ceasefire headlines.

- Supply-chain squeeze: container freight (Drewry WCI ≈ $2,800/40ft) and Baltic Dry (~3,224) are rising into early-June surcharges, pressuring Retail/Consumer Discretionary and Electronics margins.

This is structural analysis through geoeconomics and Nine Star Ki, not investment advice. Verify any actionable read with primary sources and a licensed advisor.